Hello,

As the new year continues, we reflect on 2025 as a period defined by recalibration across the capital markets. In many high-growth markets, demand reached historically strong levels; however, an unprecedented wave of supply continued to weigh on occupancy and rent growth, delaying a broader recovery in fundamentals.

We view 2026 as a year of opportunity. New deliveries are expected to decline meaningfully, and when paired with stable underlying demand, we believe this dynamic should support gradual stabilization in occupancy and a return to positive rent growth. At the same time, capital markets continue to present attractive entry points. A significant number of assets are trading below replacement cost, and with more than $160 billion of commercial real estate debt expected to mature 1 , we anticipate increased transaction activity as some owners face refinancing pressure. While not all this capital will result in distress, we do expect a growing number of managers to pursue asset sales or seek rescue capital amid ongoing NOI pressure.

In this environment, discipline remains crucial. We will continue to underwrite conservatively, remain patient in our capital deployment, and focus on opportunities that meet our risk-adjusted return thresholds. This approach is designed to allow us to protect investor capital while avoiding forced deployments and maintaining flexibility as market conditions continue to evolve.

All my best,

Gerardo Gutierrez

CEO DDelta REI

Quarterly Highlights

- The Everett, a Northwest Austin multifamily property, was converted from market-rate to a Ch.392 affordable housing structure, delivering rent-restricted units for households earning ≤80% and <60% of AMI.

- Junewood was recognized by the Austin Apartment Association as a 2025 Community of the Year award winner in the Lease-Up, 50–299 Units category, reflecting strong lease-up execution and on-site operations 2 .

Insights – Affordability Crisis

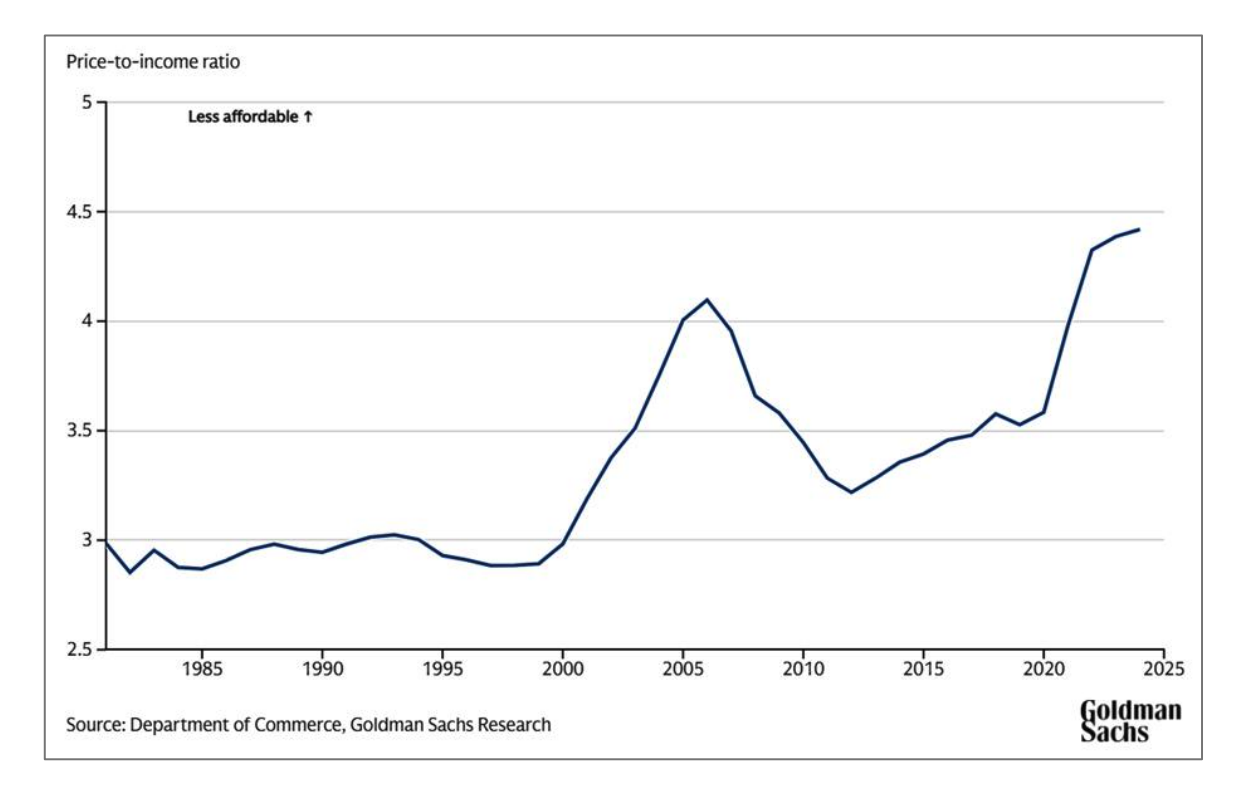

Since the Global Financial Crisis, single family housing supply growth has remained structurally constrained, making homeownership increasingly difficult to attain. Limited inventory, combined with sustained population growth in many U.S. markets, has placed persistent upward pressure on home prices. This dynamic has been further exacerbated by mortgage rates, which have remained near 20-year highs since 2022, materially increasing the cost of ownership.

As a result, home prices have continued to outpace income growth. The home price-to-income ratio has surpassed levels last observed in the early 2000s, while the average monthly mortgage payment as a share of household income has increased from below 20% prior to the pandemic to over 30% since 2022. These conditions have significantly reduced affordability for potential homebuyers.

In contrast, the cost of renting has become relatively more attractive. Recent supply pressures in several U.S. markets have led to periods of flat or negative rent growth, widening the affordability gap between owning and renting to more than $1,000 per month at the national level.

We expect this gap to remain elevated, reinforcing renter demand as leasing continues to represent a more accessible and flexible housing alternative for a growing segment of the population.

1 RCA | Q4 2025

2 The award is based on an independent evaluation of on-site operations, maintenance standards, curb appeal, and overall property condition. The Austin Apartment Association represents over 1,000 apartment communities across Central Texas and recognizes communities for operational excellence and property standards.

Source: CoStar, Goldman Sachs & RCA, Data as of Q4 2025.

Under no circumstances is this presentation to be used or considered as an offer to sell, or a solicitation of any offer to buy, any security. Any such offering may be made only by an offering memorandum that would be furnished to prospective investors who express an interest in an investment program of the type being considered, and that would describe the risks associated with an investment in the investment program.

The information contained herein is in summary form for convenience of presentation. It is not complete, and it should not be relied upon as such. The information in this presentation is provided to you as of the dates indicated and DDelta Real Estate Investments Inc. (“DDelta REI”) does not intend to update the information after its distribution, even in the event that the information becomes materially inaccurate.

The information contained herein is confidential and may not be reproduced in whole or in part nor disclosed by the recipient to any other party without our prior written consent. Certain information contained in this presentation includes calculations or figures that have been prepared internally and have not been audited or verified by a third party. Use of different methods for preparing, calculating or presenting information may lead to different results and such differences may be material.This material outlines certain characteristics of a proposed investment program. It is presented solely for purposes of discussion, to determine preliminary interest in investing in an investment program with the general characteristics described herein. There may be material changes to the structure and terms prior to the interests in an investment program being offered.

In considering any performance data contained herein, each recipient should bear in mind that past performance is not indicative of future results, and there can be no assurance that an investment program will achieve comparable results. The Fund’s target return stated herein is an aggregate, annual, compound, gross internal rate of return after the effects of debt financing (at either the Fund or property/asset level) and any fees at the property/asset level are taken into consideration. The targeted gross leveraged IRR for the Fund is based on a significant number of assumptions, including DDelta REI’s assumption that investing conditions will not deteriorate significantly over the life of the Fund. Additionally, the targeted gross leveraged IRR is calculated using assumptions and estimates regarding the Fund’s size, leverage, rate of investment and income. Actual investment pace, purchase and sale prices, and current income and other returns received on investments, investment hold periods, default and recovery rates of investments, and other factors may differ significantly from the assumptions and estimates used to calculate gross return. The gross internal rates of return presented do not reflect any management fees, carried interest, taxes and Fund expenses, which in the aggregate may be substantial. Nothing contained herein should be deemed to be a prediction or projection of future performance of the Fund.

This presentation contains forward-looking information including forward looking statements within the meaning of the U.S. Securities Act of 1933 and the U.S. Securities Exchange Act of 1934, as amended. The words “expected,” “will,” “seeking,” “project,” “may,” “might,” “would,” “should,” “could,” “contemplate,” “potentially,” “anticipate,” “target,” “intend,” “plan,” “believe,” “continue,” “focus,” “exceed,” “increased” and other expressions which are predictions of or indicate future events, trends or prospects and which do not relate to historical matters, constitute forward-looking statements. Although DDelta REI believes that the anticipated future results, performance or achievements for an investment program expressed or implied by the forward-looking statements and information are based upon reasonable assumptions and expectations, the reader should not place undue reliance on forward-looking statements and information because they involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of the investment program to differ materially from anticipated future results, performance or achievement expressed or implied by such forward-looking statements and information. Factors that could cause actual results to differ materially from those set forward in the forward-looking statements or information include but are not limited to general economic conditions, changes in interest and exchange rates, availability of equity and debt financing, and risks particular to underlying portfolio company investments.

Real estate investing involves material risks that should be carefully considered before making any investment decisions. These risks include, but are not limited to, risks related to illiquidity, changes in economic conditions, fluctuations in interest rates, financing risks, changes in supply and demand dynamics, tenant risks, environmental liabilities, and potential adverse effects of local, state, or federal laws and regulations. Real estate markets are subject to volatility and are influenced by broader economic and market conditions. There is no assurance that any investment will achieve its objectives or that any strategy will be successful.

Nothing contained herein should be construed as legal, business or tax advice. Each prospective investor should consult its own attorney, business advisor and tax advisor as to legal, business, tax and related matters concerning the information contained herein. Unless otherwise noted, all references to “$” or “Dollars” are to U.S. Dollars. All time-sensitive materials are made as of Q4 2025, unless otherwise expressly indicated.

DDelta REI is registered as an investment adviser with the U.S. Securities and Exchange Commission | SEC registration does not imply a certain level of skill or training.